The fiscal data for early 2026 tells a specific story about India. In February alone, net Foreign Direct Investment (FDI) hit a high of $4.6 billion, a number that looks great on a spreadsheet but means something far more physical on the ground.

It represents actual factories being built and real jobs being created.

But at the same time, the stock markets are swinging wildly based on the whims of Foreign Portfolio Investment (FPI), which moves with the speed of a fiber-optic cable.

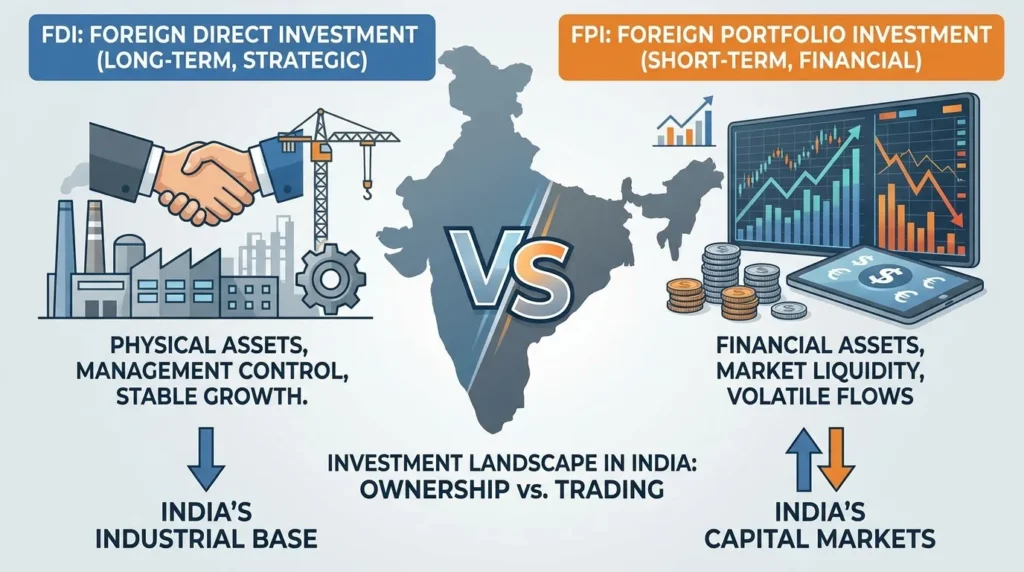

This brings us to a question often brushed over in broad economic summaries- when looking at the tug-of-war between FDI vs FPI in India.. What Is the Real Difference? It isn’t just about the money; it’s about the intention and the “stickiness” of that capital.

Defining FDI as a Long Term Strategic Commitment to Indian Growth

When a company like a global semiconductor giant decides to set up a fabrication unit in Gujarat- something we have seen accelerate in this 2026 fiscal year- they aren’t just sending cash.

They are sending engineers, intellectual property, and a long-term commitment. This is Foreign Direct Investment. To qualify as FDI, an investor generally needs to hold 10% or more of the fully diluted paid-up equity capital of a listed Indian company.

The beauty of FDI is its permanence. You can’t exactly pack up a multi-billion dollar semiconductor plant and move it overnight because the exchange rate fluctuated by two percent. In the context of the March 2026 policy updates that slashed approval times to 60 days for green energy projects.

FDI has become the bedrock of the “Make in India” push. It’s “sticky” money. It brings management expertise and a seat at the boardroom table, making the investor a partner in the nation’s industrial output.

Understanding FPI as the Liquid Pulse of the Indian Financial Markets

On the other side of the ledger, we have Foreign Portfolio Investment. Think of FPI as the “hot money.” These are the institutional investors, the hedge funds, and the pension funds buying up stocks and bonds on the National Stock Exchange. They aren’t interested in running a company or hiring workers; they are chasing yields.

By mid-2026, the inclusion of India in major global bond indices has turned the FPI flow into a massive, albeit volatile, river of liquidity. FPI is purely financial.

It provides the depth the Indian markets need to stay liquid, but it is also the first to leave when the US Federal Reserve changes its tone or global geopolitical tensions rise. It’s the difference between owning the house (FDI) and just betting on the neighborhood’s property values (FPI).

Ownership and Control as the Deciding Factors in the FDI and FPI Debate

The technical line between these two is often thinner than people realize. If an FPI increases its stake in a single company beyond 10%, the entire investment is reclassified as FDI. This 10% rule is the regulatory boundary set by SEBI and the RBI to distinguish between a passive investor and a strategic partner.

Control is the operative word here. An FDI investor wants a say in how the business is run. They want to influence the supply chain and the corporate strategy. An FPI investor, conversely, is a passenger. If they don’t like where the bus is going, they just hop off at the next stop by selling their shares.